Homeowners insurance (and other lines of insurance) rates are increasing across the country. The rate increases have drawn particular attention in areas such as Florida and Louisiana where insurance already is a larger part of peoples’ budgets and where rates have increased faster than the rest of the country.

Rising inflation, increased reinsurance costs, higher interest rates and global warming have all played a role in the increase in homeowners insurance rates across the country, as have state specific issues such as fraud and litigation abuse in Florida (which hopefully have now been addressed by Senate Bill 2A passed in 2022 and House Bill 837 passed in 2023).

Recently there have been a number of articles describing average insurance rates in Florida to an average of $6,000 or $12,000, depending on the source. Those average premiums and premium growth rates are based on small samples of data and neither are correct.

How small data sets skew the average

The gold standard for insurance price data has always been the National Association of Insurance Commissioners (NAIC). The NAIC aggregates the data that individual insurers report to statistical compilation registries such as Verisk/ISO, AAIS, and Mutual Service Office (MSO) and publishes data each year on the average price of homeowners insurance in each state. The result is accurate because it reflects data from every insurer in the US, and therefore, nearly every homeowners insurance customer.

Its most recent report was published in December 2023 and is based on 2021 data. The methodology is described in detail within the report. Previous years’ reports on homeowners insurance can be found here, going back to 1993.

The NAIC data on average homeowners insurance is used b the Insurance Information Institute (III) and has historically been often quoted by the press. More recently, since the NAIC data isn’t available for more recent years, III conducted their own survey of insurance agents and came up with an average premium of $6,000 per policy in Florida in 2023 that has been cited by a number of local Florida news outlets.

In lieu of more recent data being available from the NAIC, a number of other sources have recently been quoted by the press. For example, Insurance Journal recently republished data from Insurify showing the average premium in Florida as $10,996 in 2023 and projected to be $11,759 in 2024.

The Insurify data is based on a sample of shoppers shopping for insurance on Insurify, while the newer III data is based on a survey of insurance agents. Both are much smaller data sets than the historical NAIC data, and both are potentially skewed. For example, consumers shopping on Insurify might potentially be more risky customers who are having a harder time finding insurance, which would skew the average premium upwards.

Larger data sets provide a more accurate picture

There are some larger data sets available that are updated through 2023 that can help us determine an updated average for Florida homeowners insurance premiums:

-

The Florida Office of Insurance Regulation publishes industry data in their QUASR reports. QUASR data has gotten less accurate over time since many insurance companies exclude their data from public view by claiming they are trade secrets, so it’s not perfect, but is still based on over a million policies, a very large sample of the market.

-

Florida Citizens, the state run insurer and the largest homeowners insurer in Florida at the moment, also publishes data on the number of policies and total premiums, which can be used to compute an average.

-

Two of the larger insurance companies focused on Florida – Universal and Homeowners Choice – are public companies and include data about their average premiums in Florida in the financial reports they file with the SEC.

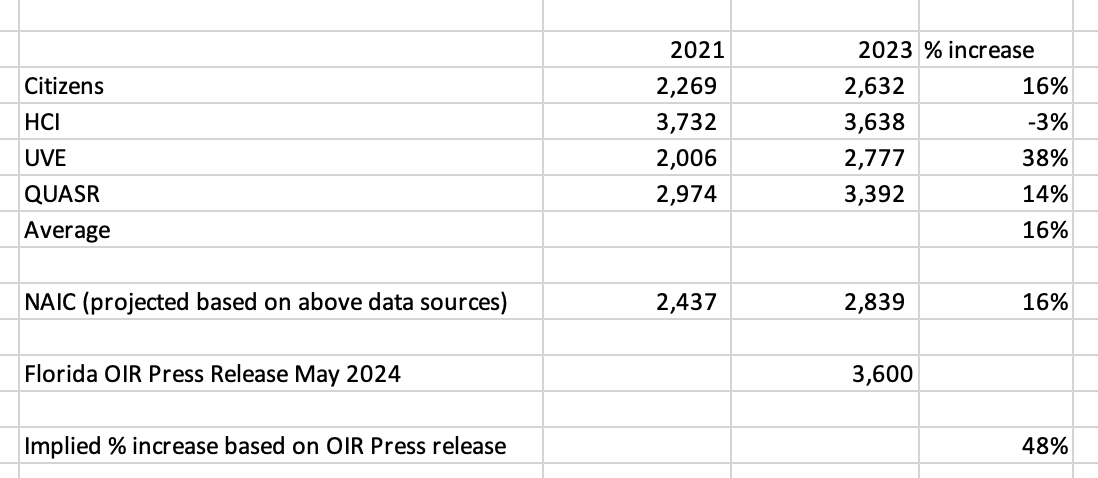

While none of those data sources are as complete as the NAIC data, they are all relatively large samples. As of December 31, 2023, the QUASR data included 1,095,201 policies, Citizens included 1,065,639, Universal had 567,893 and Homeowners Choice had 247,000. Collectively, that is a sample of almost three million policies, which is likely a lot larger than the sample size of the III survey of agents or the Insurify data set.

Furthermore, in the chart above, we can see that those data sets have pretty reliably tracked the NAIC data for a long period of time. This leads me to believe they are a reliable proxy for the overall average.

While we were writing this blog post, another data source became available, when the Florida Office of Insurance Regulation (OIR) released a market update in May 2024. That release cited “The average homeowner’s premium in the admitted market in Florida is approximately $3,600.” That data is likely based on the QUASR data collected by the OIR, but without excluding policies from the companies that claim trade secret. Unfortunately, that market update doesn’t have an equivalent from 2021, so we can’t make an apples to apples comparison of the growth rate.

On average the other four time series data sources considered comprise about three million policies, and show an increase of 16% from 2021 to 2023. When the 2023 average premiums are eventually published by the NAIC in December 2025, I expect we will also see in the ballpark of a 16% increase and an average of somewhere between $2,839 and $3,600, a far cry from the $6,000 or $12,000 numbers being quoted in the press.

Of course, many customers may pay more than that – folks who live very near the coast, who have homes with fewer windstorm mitigation features, or who have more expensive houses.

Citizens, particularly, is an interesting data source, because it’s annual rate changes are limited by the “glide path” law from 2009 that capped annual rate increases, which has left Citizens personal lines policies 57.9% below the uncapped rate needed to be actuarially sound as of the end of 2023. That is likely why Citizens is consistently lower on average than the data sources that reflect pricing of private market insurers (except UVE).

However, Citizens’ average rate has been increasing a lot, how can that be, given the glide path rule? That likely is due to the mix in Citizens changing, and moving to be more coastal. Since the loss costs and reinsurance costs have been increasing more in the very coastal areas, and Citizens is less able to respond to those rising rate costs, it likely has resulted in them becoming increasingly underpriced in those areas where premiums are higher on average, driving up their overall average. We may dig more into this topic in future posts.