You can learn a lot from the past. What can you learn from how insurance used to be?

“Know from whence you came. If you know whence you came, there are absolutely no limitations to where you can go.” -James Baldwin

It’s always fun to take a stroll down memory lane, whether it’s looking at old childhood photos, going to a local museum or reading a good historical novel. History indeed reveals the past but can often be a predictor of the future. The best part about history is the continual discovery of hidden gems; much can be learned from seemingly innocuous things that implode with fascination upon exploration.

Take homeowners insurance for instance. What could possibly be fun and enlightening about paying for something you may never actually use that requires an arduous application and claims process due to outdated systemic protocols? Well, the truth is, the insurance industry wasn’t always stigmatized as malevolent and filled with corporate greed. In fact, the concept of homeowners insurance transpired out of the Great London Fire in 1666. This unprecedented blaze destroyed over 13,000 homes, and it’s estimated over 70,000 of London’s then 80,000 homes endured damage as well.

As such, fire insurance was born and essentially paved the way for present-day homeowners insurance. Fires were rather common because wood was the primary material to build homes and people used gasoline stoves and candles to make light. This equaled an inevitable recipe for disaster. Our ancestors started off by isolating just one peril, fire, and then slowly began to offer various other forms of insurance protection.

In 1732, fire insurance was introduced to the United States but didn’t really garner popularity until the next century.

What did a typical policy look like in the 1800's?

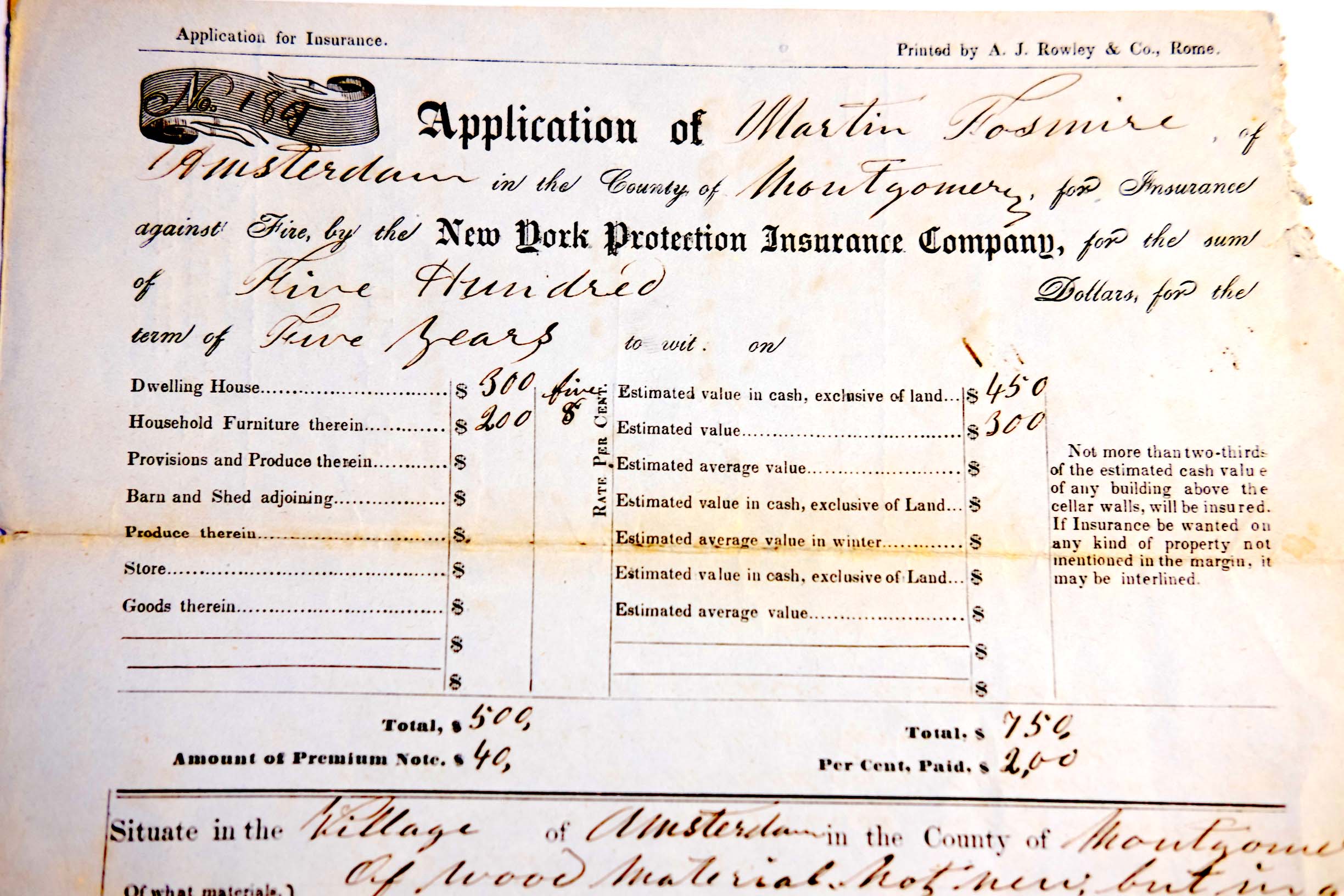

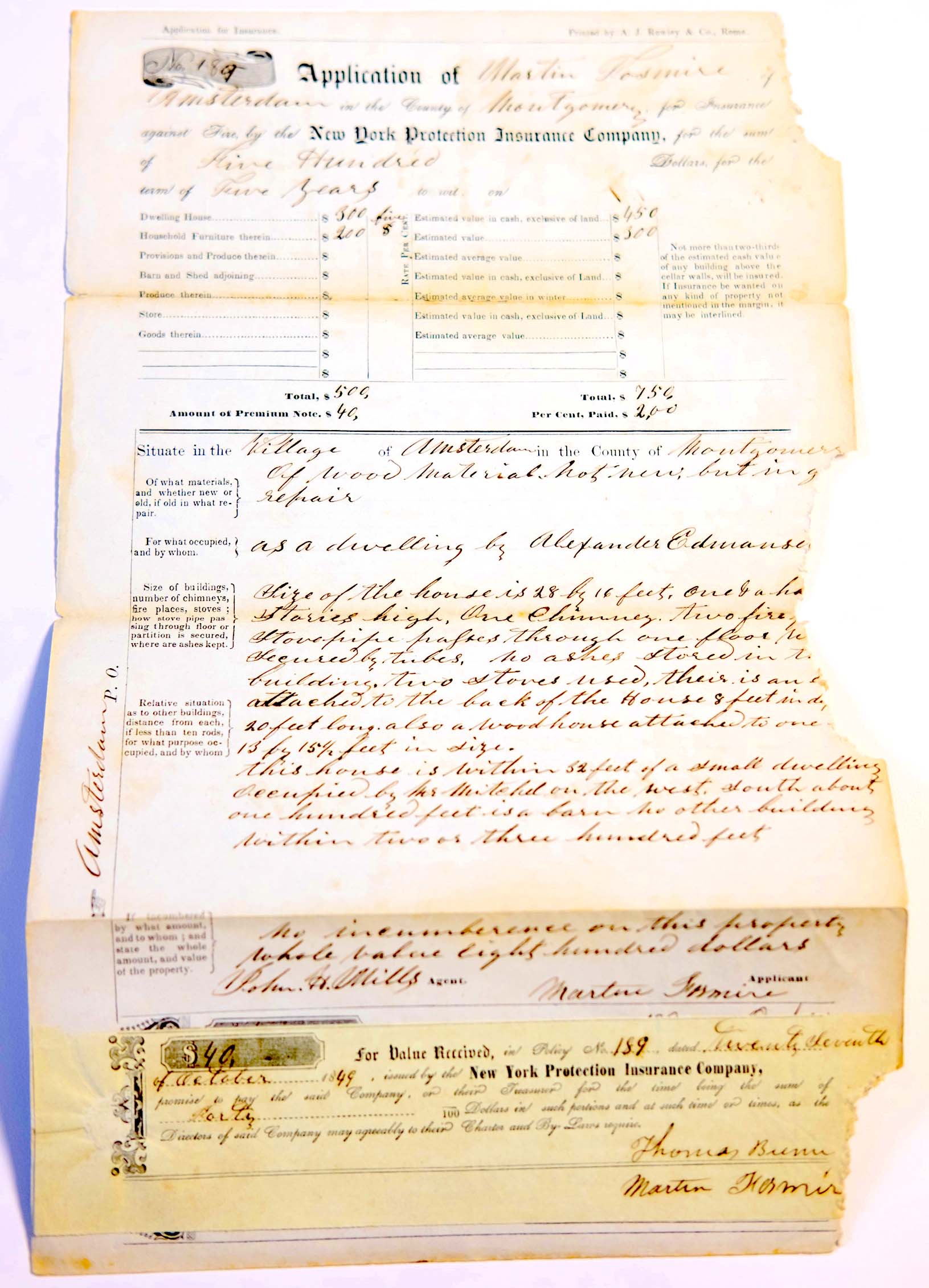

Actual insurance policy from 1849 with $500 worth of fire coverage for a $40 premium with a policy duration of 5 years.

Actual insurance policy from 1849 with $500 worth of fire coverage for a $40 premium with a policy duration of 5 years.

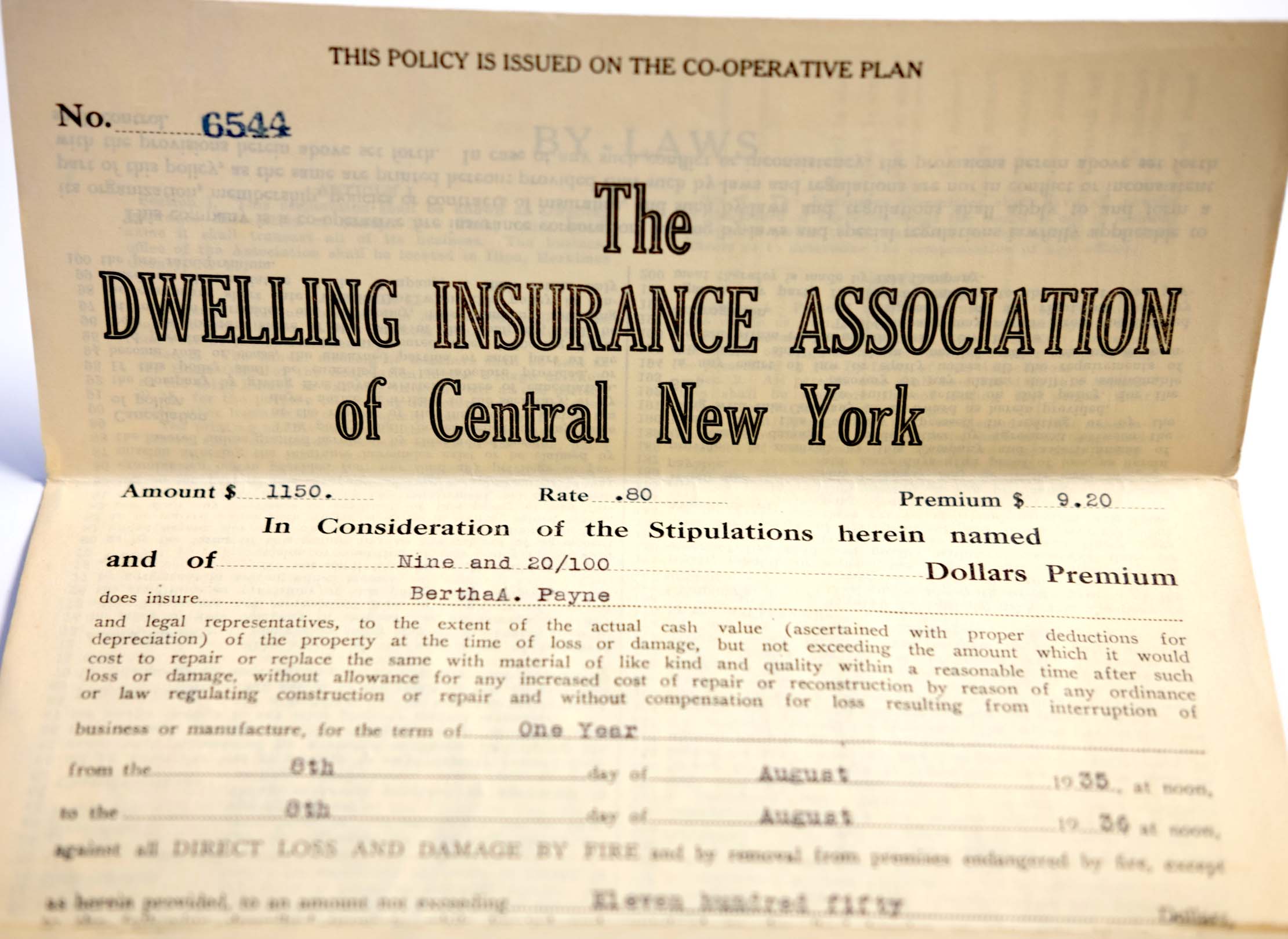

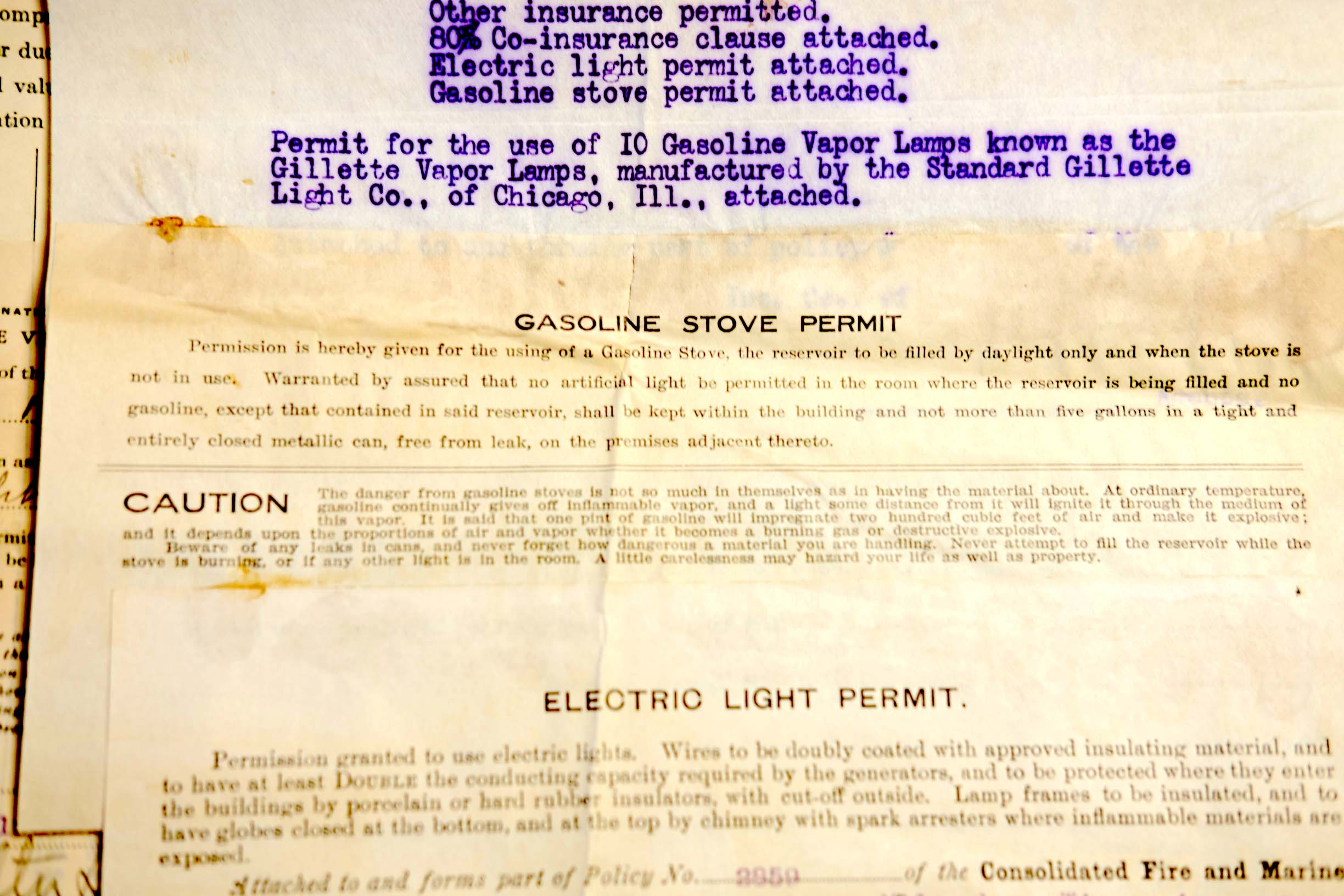

For $5 in 1849, an individual could get a $500 fire policy. Prices in 2017 are 2985.4% higher than prices in 1849, so $5 is equivalent to $154.27, and $500 is equivalent to $15,426.78. That doesn't sound too bad at first glance, however, many insurance companies at the time did not insure up to the full cash value and only offered a percentage of the value of the property. This was only for the structure of the home as well. Again, as history progressed, more and more types of policies were added such as for furniture (which predates today's personal property coverage), gas stove permits, electric light permits, lightning, and marine coverage.

This is an actual handwritten insurance policy from 1849

This is an actual handwritten insurance policy from 1849

To give a little context, the average worker in the mid-1800s earned about $1-$2 a day. Work back then was very different than today; folks didn’t go to the same place, punch in, and work 40 hours a week. Things were very sporadic and unpredictable. As such, the average person earned $10-$20 a month. In 2017 standards, that’s about $30-$60 a day or $595-$620 a month. Back then folks were paying about a week or two’s worth of salary on fire insurance.

In 2017, the average cost of a homeowner’s insurance policy nationally was $1,082. The average income for a single person according to the most recent US Census data in 2014 was $34,940. Since women did not work in the 1800’s the fairest comparison is with a single today. So essentially, the same applies over 150 years later, a homeowner’s insurance premium is still about 1-2 weeks’ salary.

So what did a house cost in the 1800s?

According to the National Park Service, in 1870 land cost $5/acre (avg. 160 acres) a 4 ROOM house was 32’x40’ and cost $700, a TWO-room house was 16'x22' and cost $300, and a shanty 8'x10' (1room/dirt floor) was $25. Remember, a $5 premium could garner $500 worth of fire coverage but didn't necessarily cover the full replacement. The most challenging thing plaguing consumers at the time was the claims process. The industry was essentially self-regulating with very little governmental intervention. Folks were getting scammed and so were the insurance agencies. Arson was a very big problem as everyone was looking for a payout. Many insurance companies were not able to pay out claims as they had inadequate funds, just like a present-day Ponzi scheme.

The main takeaway from looking back upon the history books is to see how society has evolved and get an understanding of the complexities and unpleasantries of the homeowners' insurance industry in general. Many people were severely burned during that time by unscrupulous practices paving the way for increased governmental oversight on both the federal and state levels. Consumer protectionism, customized policies, and comprehensive policies were nonexistent at the time.

Insurance companies have historically had immense leverage in society and are perceived as a necessary evil. Without homeowners insurance all the homes affected by hurricanes, earthquakes, fires, and any other devastating act would remain in ruins, cities would be destroyed, and states and countries would be a lot worse off.